The arrival of steel prices in the traditional peak season is expected to rebound

Suitable for quenched steel, tempered steel, annealed steel, cold and hard casting,malleable cast iron, hard alloy steel, aluminum alloy, copper alloy, bearing steel etc. Also suitable for surface quenched steel, surface heat treating and chemical treating materials, sheet, zinc layers, chrome layers, tin layers etc.

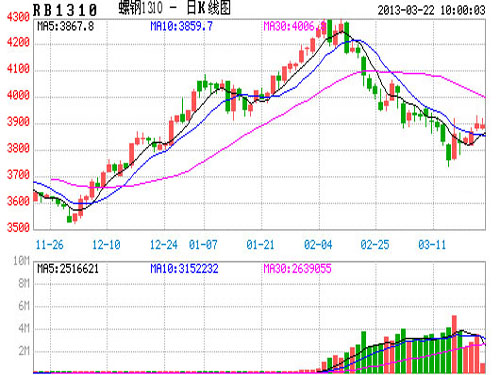

Hardness Testing ,Tele Brinell Hardness Tester,Brinell Hardness Test Scale,Portable Rockwell Hardness Tester TROJAN (Suzhou) Technology Co., Ltd. , https://www.trojanmaterials.com First, the February market review February coincided with the Chinese New Year, the steel market finished lower, ushered in high adjustments. At the beginning of February, the period steel market oscillated higher and continued the strong pattern at the end of January. On the 5th of the rb1305 main contract, the highest touched 4235 points, reaching a new high since the end of April last year. After the year, the main force gradually changed its month to rb1310. At the same time of shifting positions on the month of exchange, the price of high-grade steel was pulled back. On the 27th, the rb1310 fell to 3950, and the month-end closed at 4053. The monthly line closed negative and closed down 3.25%. The fall in the price of steel in the second half of the month has also been affected by seasonal factors. Since the listing of steel in the period, the monthly line in February has been negative every year. Since January’s advance overdrafts have risen, the downstream demand has not yet started in February. The price has fallen into a natural probability event.

First, the February market review February coincided with the Chinese New Year, the steel market finished lower, ushered in high adjustments. At the beginning of February, the period steel market oscillated higher and continued the strong pattern at the end of January. On the 5th of the rb1305 main contract, the highest touched 4235 points, reaching a new high since the end of April last year. After the year, the main force gradually changed its month to rb1310. At the same time of shifting positions on the month of exchange, the price of high-grade steel was pulled back. On the 27th, the rb1310 fell to 3950, and the month-end closed at 4053. The monthly line closed negative and closed down 3.25%. The fall in the price of steel in the second half of the month has also been affected by seasonal factors. Since the listing of steel in the period, the monthly line in February has been negative every year. Since January’s advance overdrafts have risen, the downstream demand has not yet started in February. The price has fallen into a natural probability event.

In terms of quantity and energy, the main force basically completed the shift from rb1305 to rb1310 in February. As of February 28, the trading volume and open interest of the thread index were 41.861 million hands and 1.337 million hands respectively, a decrease of 10.96 million and 18.4 million hands respectively from the end of January. The decline in transaction volume in February was also due to the Spring Festival holiday, and the number of trading days was only 15 days. In addition, in February, especially after the holiday season, with the fall in the price of steel, the overall position is showing a downward trend. After the price is higher, especially at more than 4100 points, the degree of participation in funds has decreased. It can be seen that the high price adjustment, the market The outlook for the market outlook is not clear.

In February, the steel spot market oscillated ahead and remained strong. Before the Spring Festival, the market gradually entered a state of rest and the transaction volume was light, but the price was stunned by excitement and showed a state of immeasurable airlift. After the holiday, the price rose and the price continued to rise. As of February 28, the mainstream quotation of HRB400 in Shanghai market was 3,850-3,900 yuan / ton, which was a cumulative increase of about 50-100 yuan / ton compared with the price at the end of January. It was entirely a firm support for the outlook that the stock price is expected to be well supported. Regarding the price adjustment of steel mills, although domestic terminal demand was at the lowest point of the year in February, domestic steel mills have substantially increased their overall ex-factory prices due to cost pressures and expectations for the outlook. In early February, construction steel manufacturers substantially increased the ex-factory prices and remained stable in the mid-to-late months. In which the dominant steel mills in East China, Shagang, Yonggang and Zhongtian, raised the prices of rebar and wire rods by RMB 200/tonne and RMB 100/tonne, respectively, and remained stable in the middle and later quarters. At present, in some regions, the price of steel mills has reverted to the market price, which is obviously upside down, and is about 50-150 yuan/ton.

Second, the demand analysis: the arrival of the traditional peak season, the downstream demand for steel will slowly stabilize in March rebound 2.1 Real estate development investment growth is slower than expected, as in previous years, as in February this year, the National Bureau of Statistics did not publish real estate development investment data. Since 2012, the decline in the sales volume of commercial housing in China continued to narrow and the first positive growth in the year in November, and the volume of transactions throughout the country in December and January was generally enlarged. First-tier cities such as Beijing rose in volume and price, and the country was in the spring. Re-transmit the signal of real estate regulation overweight. First, since January, housing policies in several cities including Kunshan, Dongguan, and Jinhua have frequently tightened, followed by the State Council executive meeting held on February 20 to specifically regulate the real estate market. On the evening of March 1, the State Council The office issued more stringent rules and regulations.

“Overall, the real estate regulation has been further upgraded and the regulation has slightly exceeded expectations. The regulation is mainly focused on the following aspects:

1. Strict supervision over the control of house prices, again referring to the local accountability system, this depends on how local government price targets are set and the follow-up supervision;

2. Increase the limit of purchase and limit the loan, increase the coverage of the city;

3. The adjustment and adjustment of the second-home suite, the second-home down payment ratio and the ** interest rate will be tight, including the first-tier cities and some second-tier cities where housing prices are rising faster;

4. A 20% income tax will be levied on the value-added portion of second-hand housing sales. This will undoubtedly have a second-suite demand in the short-term and will continue to push up housing prices (including new and second-hand housing) in the long term;

5. Strengthen the supervision of intermediate links and strictly implement the previous policies.

We believe that the introduction of the “Detailed Rules†will bring down the real estate market. The first priority will be the volume of transactions. It is expected that the residential turnover will fall from a high level in the next 1-2 quarters, and the price will also fall with the volume. The increase will slow down significantly, but we think the possibility of a significant drop in house prices is less likely, because although the “Detailed Rule†mainly lies in managing demand and curbing real estate demand, the 20% tax also inhibits supply. In addition to this, in 2013, the tight supply pattern of new houses did not change, and there was no significant drop in prices. However, severe regulation and control will continue to cool down the real estate that has continued to heat up since June last year. Demand will also be curbed and the enthusiasm of developers for land acquisition will also be reduced. We feel that the real estate market trend has officially entered the “pessimistic expectations†direction mentioned in our annual report. . "(See [China Securities Macro Weekly 20130304 - Global Macro Weekly Issue No. 2]) Although we maintain our previous view, the trend of real estate continues to stabilise and pick up in March will not change, but real estate development and investment growth will slowly increase. More sexual.

2.2 Railway infrastructure investment declined seasonally at the beginning of the year, but the year-on-year increase was quite alarming. In terms of infrastructure, the latest statistics released by the Ministry of Railways showed that railway fixed asset investment completed 20.939 billion yuan in January 2013, an increase of 8.711 billion yuan year-on-year, an increase of 70.9% year-on-year Among them, the capital construction investment was 14.175 billion yuan, an increase of 5.443 billion yuan over the same period of last year, an increase of 62.3% over the same period of last year, which was an alarming year-on-year increase. The investment amount completed in January this year is not high compared with the annual investment of 650 billion yuan. From past experience, the Ministry of Railways' fixed-asset investment and capital construction investment are the lowest values ​​in the whole year, and this year will still be the lowest value. Continue this feature.

Workers and peasants in the four major new businesses in China Construction Bank amounted to RMB 250 billion, which was much higher than the RMB 180 billion in the whole month of February last year. A large part of the credits put down on infrastructure construction such as railways, highways, and rail transit. Above. In short, if the three sources of capital in the central budget, the issuance of bonds, and the banking sector can be implemented as scheduled, then the Ministry of Railways’ task this year will be relatively easy. However, the Ministry of Railways is difficult to get rid of the situation that the debt ratio is increasing year by year and tax profits are decreasing year by year. Statistics show that the liabilities of the Ministry of Railways in 2010, 2011 and the first half of 2012 were 18,918 billion yuan, 2,412.7 billion yuan, and 2,255.7 billion yuan respectively. The rates were 57.44%, 60.63% and 61.08%, respectively, and the after-tax profits were 15 million yuan, 31 million yuan and -88.1 million yuan respectively.

In summary, the tendency of real estate investment to stabilize and pick up after the year does not change, but there will be no significant increase under the restriction of control policies, and the upward process will be relatively slow. The seasonal decline in railway fixed assets and infrastructure investment will basically meet our expectations, but The year-on-year increase was still impressive, and the slow recovery in the latter period was still a high probability event. In general, we tend to see the slowdown in the downstream demand for steel in March as the traditional peak season arrives.

3. Supply analysis: With the arrival of the peak season, the output is still high, and the social inventory or spikes have fallen. According to the latest data from the Steel Association, the domestic crude steel output in January 2013 is estimated at 59.3 million tons, an increase of 4.6% year-on-year; January domestic crude steel The average daily output was 1,913,300 tons, which was 0.8% higher than the 1,892,200 tons estimated in December 2012, showing little increase. In the first half of February 2013, the average daily output of crude steel for key large and medium-sized enterprises was 1,701,400 tons, which was a 6.1% increase on a month-on-month basis. The average daily crude steel production in the country in early February was estimated at 1,988.9 thousand tons, up by 4.4% from the previous month. The average daily output of crude steel and the average daily average output of crude steel in the major steel enterprises estimated by the China Iron and Steel Association have reached historically new high levels. In the context of better execution of pre-orders and continued rise in ex-factory prices, the steel mills' enthusiasm for production was generally high. In early February, the country’s crude steel production rebounded rapidly. At the same time, according to the survey, the steel mills mostly maintained normal production during the Spring Festival, and some key steel mills also significantly accelerated the pace of production, and the market demand during this period was close to the vacuum, which will also lead to increasing pressure on domestic steel supply in the later period.

Under normal circumstances, the output of steel mills will decline in the fourth quarter of the year (this has already been mentioned in the annual report and the February monthly report); after the spring of the year, affected by seasonal factors, steel mills will generally start production at the beginning of the year. Second, from March to March in the beginning of the year, it was the traditional peak season. Strong expectations of steel mills' demand will drive output higher. This is an important reason for the strong recovery in February. In March, the two influencing factors did not change, so steel mill production will not be lower than February, or even slightly increased.

The source of railway construction funds mainly comes from banks and the issuance of bonds. In 2012, the Ministry of Railways issued 200 billion yuan of bonds, and the banks also had more than 200 billion yuan. The above two accounts for more than 70% of their total amount. According to the latest news from the Ministry of Railways, in the next few years, we will continue to increase investment in railway construction budgeted by the central budget and implement the issuance scale of 150 billion yuan in railway construction bonds annually. In 2012, the budget of the central budget increased by 40 billion yuan. Although it does not account for a large proportion of the total amount, it is also significantly more than the amount of billions of yuan previously planned. It is expected that the amount of funds within the budget will increase this year. .

In terms of social inventory, as of February 22, the social inventory of rebars and wire rods was 962.06 and 276.35 million tons, respectively, an increase of 2,994,100 tons and 1,149,800 tons on a month-on-month basis. The monthly increase reached 45.6% and 71.3%, regardless of inventory. Absolute or monthly increases have hit record highs. In the annual report, we mentioned that the volatility of building materials' social inventories showed obvious seasonal characteristics. After eliminating seasonal factors, the rebar and wire social inventories at the end of February were still increased by about 9% and 7% respectively compared with the same period of last year. . The rapid increase in social stocks after this year’s holiday season was due to factors such as the relatively cold weather, lack of full-scale downstream demand, and the steel traders’ having to obtain goods from the steel mills according to the agreement. These are basically in line with what we expected in the February monthly report. of. However, the social inventory of building materials hit a record high, exceeding our expectations. This was mainly due to the rapid increase in steel production and the relative lack of downstream demand. At present, the output of steel mills remains high, and the short-term release of downstream demand is not enough to absorb stocks. The trend of rising social stocks may continue, but in the second half of March, as the demand picks up, social stocks may increase. High down.

From the steel mill inventory situation, China Iron and Steel Association statistics in late January, the key steel enterprises steel inventory was 10.59 million tons, a decrease of 1.23% in the Central chain. According to the survey, during the Spring Festival, most of the steel mills are based on normal production. The steel mills have very little maintenance to reduce production, and inventory in the plant area will increase slightly in February. This is in line with what we anticipated in the February monthly report. From the end of each year to the second and third months of the next year, the steel stocks of steel enterprises generally increase. Decrease in steel inventories in December 12 was the result of steel mills' initiative to destock inventory, and inventory of steel companies may rise in January-February this year. In summary, after the Spring Festival, with the arrival of the traditional peak season, the output of steel mills will maintain a relatively high level, and it is expected that the daily production of crude steel will remain at 195-200 million tons in 2-3 months. As in previous years, the year-on-year high of building materials social inventory will appear from the end of February to the beginning of March. Therefore, the social inventories of building materials may decline in March.

IV. Analysis of raw material prices: Costs will remain high In February, the prices of raw materials such as iron ore and coke will rise and fall in different markets, showing mixed performance. The price of imported iron ore rose continuously before the holiday and fell after the holiday. On the 20th, 62% of the Australian ore fines' external quotation reached the highest price of $158/ton during the month, and they oscillated after the end of the year. As of the 28th, the quotation was $152/t, which was a slight increase of about $4/t from the end of January. According to statistics, as of February 22, the stock of domestic iron ore ports reached 78.9 million tons, which was about 1.5 million tons less than that at the end of January. As a result of the restocking actions of steel mills, the inventory of ports has dropped. At the same time, the import of iron ore in January was 65.53 million tons, an increase of about 10% year-on-year, a decrease of 7.6% from the previous month, which was in line with seasonal characteristics. In February, the domestic iron ore price continued to rise, and it rose by RMB 30/t from the end of last month. After the holiday, the price of imported ore continued to rise, forming a certain pull on the trend of domestic mines. However, most of the current steel mill inventory can be maintained until the end of the month, so there is little action on the procurement side, taking a wait-and-see attitude, the market volume is light. In February, the market price of steel billets rose first and then declined. On February 19th, the billet price of Tangshan's carbon bills reached 3,330 yuan/ton, which was the high point in the month and fell steadily in the end of the next year. As of the 28th, the price was about 3,250 yuan/ton. By the end of January, it was down by about RMB 50/t. In February, affected by the Spring Festival, the sales of steel billets were sluggish. After the holiday, the stock of billets in Tangshan increased significantly and obviously exceeded the level of the same period of last year, which exerted greater pressure on the market trend. In February, the coke market changed from strong to weak and remained strong before the holiday. After the holiday, due to the pre-holiday restocking operation of the downstream steel mills, the company’s inventory was fair, and the demand for coke procurement weakened. In the context of some steel mills taking the lead in price adjustment, the focus of the coke market has shifted downwards. On February 28, the secondary metallurgical coke price in Tangshan was 1,725 ​​yuan/ton, a slight decrease of 10 yuan/ton from the end of January. (For an analysis of the coke price, please refer to [China Metals (Coke) March 2013 Report]. According to our estimation, as of February 28, the cost of building materials production was about RMB 3,700-3,750/ton, which was basically flat compared with the end of January. In general, raw materials in the upstream of steel products rose sharply in February, achieving price recovery and a rational return. With the arrival of the traditional peak season for domestic steel market in March, it is expected that the raw material prices will maintain a high level of steel costs.

V. Market Outlook in March 2013 The spot price of the steel spot market in February was stronger, which was mainly supported by the good expectations for the later period; the steel market showed a sharp decline, ushered in high adjustments, and the price of steel was more rational. return. For the later period, we generally continue the previous point of view, with the arrival of the traditional peak season, the trend of rebar demand in the downstream of rebar will be stronger than in February, but the process of real estate control policies to increase or regain demand is slower than expected; we also agree The output has also remained high. With the social inventory already high, the pressure on supply has gradually increased, which will inhibit the room for price increase. Therefore, in March, steel prices may rebound after the first adjustment, but the rebound height is also relatively limited. In response to the strategy, it is recommended that the main contract rb1310 should maintain short-term operation or wait and see before the trend is clear.