September hot rolled coil prices continue to rise

In August, the prices of hot-rolled coils continue to increase, and the order quantity of the contractors for the leading steel mills decreased. The phenomenon of resource interruptions in various regions continued, and the total amount of hot-rolled inventories in 29 key domestic cities of Lange Steel also counted. Has been almost equal to the low point of this year, so that the market price will continue to pull up. In spite of the effect of the end of month effect, the arrival of the HRC market has accelerated in the near future. However, the order quantity given by the first-line steel mills to the agreement-holders still declined in September. The arrival of resources will still be unsatisfactory, and the cost support will accelerate. The price of raw material iron ore bottomed out in July and accelerated in the first half of August, further raising the production costs of steel mills, and continuing to push up the center of gravity of finished products through the price transmission mechanism. According to the data of the General Administration of Customs, the import volume of iron ore in China increased by a large margin in July. According to the production cycle of steel plants, the increase in production costs of steel mills will be extended to September in accordance with the financial calculation cycle. In the middle and early days. Therefore, whether it is from the reduction of resources in September to see the situation or from the cost side of the support factors to consider, September finished coil prices will still have a room for improvement. ASME So Flanges,Carbon Steel Plate Flanges,Astm A105 Flange,Carbon Steel Pipe Flanges Cangzhou Youlong Pipe Fitting Manufacturing Co., LTD , https://www.ypco88.com

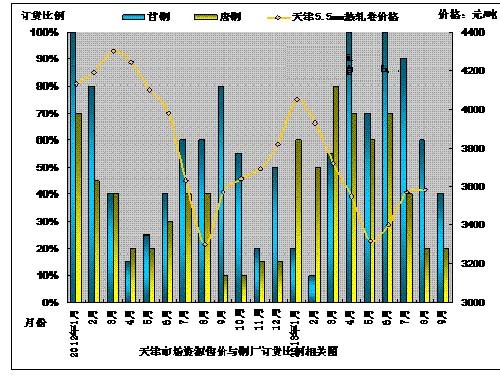

I. The pressure on resource supply by steel mills continued to decline in September. 1. According to the monitoring data of Lange Steel, the changes in the ordering ratio of steel mills have a negative correlation with changes in steel prices.

2. In September 2013, the ordering ratio of hot rolled coil resources in Tangshan Iron and Steel Co., Ltd. of the Tianjin market continued to remain low, and the ordering ratio of Shougang's hot-rolled coil board resources remained stable. Among them, the ordering ratio of Shougang to the agreement accounters dropped from 60% to 40%. The export orders will continue to maintain a good influence. The regional hot coil ordering ratio in Tianjin continues to remain low at 20%, while the Tangshan region gives orders to the agreement accounters to maintain 25% of the agreement volume, which is negatively related to the trend of steel prices according to the ordering ratio. In terms of the relationship, it is predicted that the market price of hot-rolled coils in Tianjin in September will continue to increase compared with August.

3. In 2013, the average orders for hot rolled coils of the five northern steel plants such as Shougang, Tangshan Iron and Steel, Handan Iron and Steel (Shandong), Anshan Iron and Steel and Benxi Iron & Steel were 41% in September, which was 5 percentage points lower than that in August, indicating the circulation of HRC in September. The pressure on market resources continued to weaken compared with August, and the sales pressure of HRC in September was less than that in August. However, the average order ratio decreased by 13 percentage points from August, which means that the price increase in September was significantly less than in August.

Second, raw materials and ore prices rebounded and pushed up steel production costs. As the price of finished products rose, steel production enthusiasm has risen. The General Administration of Customs data showed that the total import of iron ore in July increased significantly. The imported mines and domestic mines began to recover in full in July. 61.5% of Australia's PB powder prices reached US$141 in mid-August, hitting a new high in five months; 63.5% of India's price of powder was also increased from US$131 in early August. It rose to 139-141 US dollars, or up 8%, reaching a new high in nearly 4 months. The sharp rise in the price of imported ore has led to a sharp rise in the cost of steel production in China, which has pushed up the production cost of finished material resources through the price transmission mechanism.

First-line steelmakers Baosteel, Wuhan Iron and Steel, Hegang, and Shougang have all raised the ex-factory prices in September. Angang and Benxi Steel's ex-factory prices have been relatively high in August, and they have been relatively stable in September. The momentum of steel market cost support has continued to increase. Helping steel prices continue to rise.

In addition, according to the production cycle of steel mills, the increase in production costs of high-value mines for steel mills must be reflected in the financial costs of the steel mills at least from late August to early September. Therefore, we estimate that steel mills will have a After the ex-factory price of resources is substantially raised, the tone of the increase will continue in October. However, according to our data from Lange.com, the market price changes will generally precede the adjustment of the steel mill's ex-factory price. Therefore, we predict that the price of hot-rolled coil will still be expected to be devalued in September.

Third, the cost price and market price upside down significantly in September there are upward corrections in demand for hot coils In addition, with the ex-factory resource costs significantly increased, the arrival costs of new resources in September also significantly higher, with the current mainstream market in major regions offer In comparison, there is a clear floating difference. Tianjin market 5.5mm Shougang, Chenggang, Tangshan Iron and Steel offer in the 3580-3600 yuan or so, and in September the operating cost of steel factory production resources has reached 3,700 yuan, toss away bulk preferential and cash and shipping compensation and other preferential policies, the lowest cost Has been more than 3655 yuan, with the current market price is also a difference of 75 yuan. Similarly, the floating difference between the minimum arrival cost of Shanghai Steel Resources in September and the current market price in September is close to RMB 200. The floating price of new steel resources in September and the current market price is still 100 Yuan above (here does not include year-end rebates). In the Lecong market, the arrival costs of new resources for Angang in September are also higher than the current market price. According to the depriving characteristics of capital and the operating characteristics of products, we have reason to consider that there will be an upward revision of the hot rolled coil spot market price in September.

Fourth, the European and American economies recovered from the stable recovery of the steel industry's export orders. Thanks to the stimulation of global loose policies, the global manufacturing prosperity index in July rebounded. In particular, the performance of manufacturing industries in Europe and the United States is the most prominent. After the Eurozone-produced boom index returned to the expansion zone in July, the initial value of PMI in August rose sharply to 51.3, reaching the highest level in 26 months. After adjusting for seasonal factors, the US manufacturing PMI index rose to 53.9 in August, the highest since March. The Fed **Bernanke also expressed in the recent meeting of interest rates to reduce QE in the future, which also implies that the recovery momentum of the current US manufacturing industry has been recognized by the market. At the same time, the prosperity index of China's manufacturing industry also rebounded significantly. The initial value of China's manufacturing PMI released by HSBC in August was 50.1, which was higher than the July final value of 47.7, the largest increase in three years, indicating that China's manufacturing industry has also performed Back to temperature. The economic recovery in Europe and the United States has also led to the continuation of the export momentum of China's domestic steel mills. Although China’s steel exports declined in July, it remained above 5 million tons. The recent export orders of Taigang, Tangshan Iron and Steel, Handan Iron and Steel, and Benxi Steel's coils have maintained good conditions, which has also led to a continued decline in the amount of domestic resources. In the production cycle of steel mills, they usually take the first guarantee after export and then domestically. Both Handan Iron and Steel and Taigang are semi-monthly steel products, and the production of ordinary carbon steel in the second half of the month is the main one, which has also led to the release of the domestic plate resources. Less than half of the month, the arrival of the second half of the state. Take Tangshan Steel as an example. Throughout July and August, the hot-rolled production line of Tangshan Iron and Steel Co., Ltd. was mostly based on thin gauges of 1.8mm, 1.5mm, and 2.0mm, while the export of thin gauge accounted for more than 50% of the export volume of Tangshan hot-plates. This led to a serious shortage of resources in the Tangshan region, and the rapid increase in iron and steel equipment resources in the market. At the same time, the export of long products of Tangshan Iron & Steel exceeded 130,000 tons in the first half of the year, and the export of cold rolled steel was 680,000 tons, an increase over the same period of last year. In addition, the difference between domestic and foreign prices is still maintained, China's export price advantage still exists, but also the main factor supporting the export of HRC.

In summary, the price of hot-rolled coils in September is expected to continue the uptrend, but the increase may be less than in August.